Returns forecasts and prediction intervals for a generalized random walk model.

rwf() is a convenience function that combines rw_model() and forecast().

naive() is a wrapper to rwf() with drift = FALSE and lag = 1, while

snaive() is a wrapper to rwf() with drift = FALSE and lag = frequency(y).

Usage

# S3 method for class 'rw_model'

forecast(

object,

h = 10,

level = c(80, 95),

fan = FALSE,

simulate = FALSE,

bootstrap = FALSE,

npaths = 5000,

innov = NULL,

lambda = object$lambda,

biasadj = FALSE,

...

)

rwf(

y,

h = 10,

drift = FALSE,

level = c(80, 95),

fan = FALSE,

lambda = NULL,

biasadj = FALSE,

lag = 1,

...,

x = y

)

naive(

y,

h = 10,

level = c(80, 95),

fan = FALSE,

lambda = NULL,

biasadj = FALSE,

...,

x = y

)

snaive(

y,

h = 2 * frequency(x),

level = c(80, 95),

fan = FALSE,

lambda = NULL,

biasadj = FALSE,

...,

x = y

)Arguments

- object

An object of class

rw_modelreturned byrw_model().- h

Number of periods for forecasting. Default value is twice the largest seasonal period (for seasonal data) or ten (for non-seasonal data).

- level

Confidence levels for prediction intervals.

- fan

If

TRUE,levelis set toseq(51, 99, by = 3). This is suitable for fan plots.- simulate

If

TRUE, prediction intervals are produced by simulation rather than using analytic formulae. Errors are assumed to be normally distributed.- bootstrap

If

TRUE, then prediction intervals are produced by simulation using resampled errors (rather than normally distributed errors). Ignored ifinnovis notNULL.- npaths

Number of sample paths used in computing simulated prediction intervals.

- innov

Optional matrix of future innovations to be used in simulations. Ignored if

simulate = FALSE. If provided, this overrides thebootstrapargument. The matrix should havehrows andnpathscolumns.- lambda

Box-Cox transformation parameter. If

lambda = "auto", then a transformation is automatically selected usingBoxCox.lambda. The transformation is ignored if NULL. Otherwise, data transformed before model is estimated.- biasadj

Use adjusted back-transformed mean for Box-Cox transformations. If transformed data is used to produce forecasts and fitted values, a regular back transformation will result in median forecasts. If biasadj is

TRUE, an adjustment will be made to produce mean forecasts and fitted values.- ...

Additional arguments not used.

- y

a numeric vector or univariate time series of class

ts- drift

Logical flag. If

TRUE, fits a random walk with drift model.- lag

Lag parameter.

lag = 1corresponds to a standard random walk (giving naive forecasts ifdrift = FALSEor drift forecasts ifdrift = TRUE), whilelag = mcorresponds to a seasonal random walk where m is the seasonal period (giving seasonal naive forecasts ifdrift = FALSE).- x

Deprecated. Included for backwards compatibility.

Details

The model assumes that

$$Y_t = Y_{t-p} + c + \varepsilon_{t}$$

where \(p\) is the lag parameter, \(c\) is the drift parameter, and \(\varepsilon_t\sim N(0,\sigma^2)\) are iid.

The model without drift has \(c=0\). In the model with drift, \(c\) is estimated by the sample mean of the differences \(Y_t - Y_{t-p}\).

If \(p=1\), this is equivalent to an ARIMA(0,1,0) model with an optional drift coefficient. For \(p>1\), it is equivalent to an ARIMA(0,0,0)(0,1,0)p model.

The forecasts are given by

$$Y_{T+h|T}= Y_{T+h-p(k+1)} + ch$$

where \(k\) is the integer part of \((h-1)/p\). For a regular random walk, \(p=1\) and \(c=0\), so all forecasts are equal to the last observation. Forecast standard errors allow for uncertainty in estimating the drift parameter (unlike the corresponding forecasts obtained by fitting an ARIMA model directly).

The generic accessor functions stats::fitted() and stats::residuals()

extract useful features of the object returned.

forecast class

An object of class forecast is a list usually containing at least

the following elements:

- model

A list containing information about the fitted model

- method

The name of the forecasting method as a character string

- mean

Point forecasts as a time series

- lower

Lower limits for prediction intervals

- upper

Upper limits for prediction intervals

- level

The confidence values associated with the prediction intervals

- x

The original time series.

- residuals

Residuals from the fitted model. For models with additive errors, the residuals will be x minus the fitted values.

- fitted

Fitted values (one-step forecasts)

The function summary can be used to obtain and print a summary of the

results, while the functions plot and autoplot produce plots of the forecasts and

prediction intervals. The generic accessor functions fitted.values and residuals

extract various useful features from the underlying model.

Examples

# Three ways to do the same thing

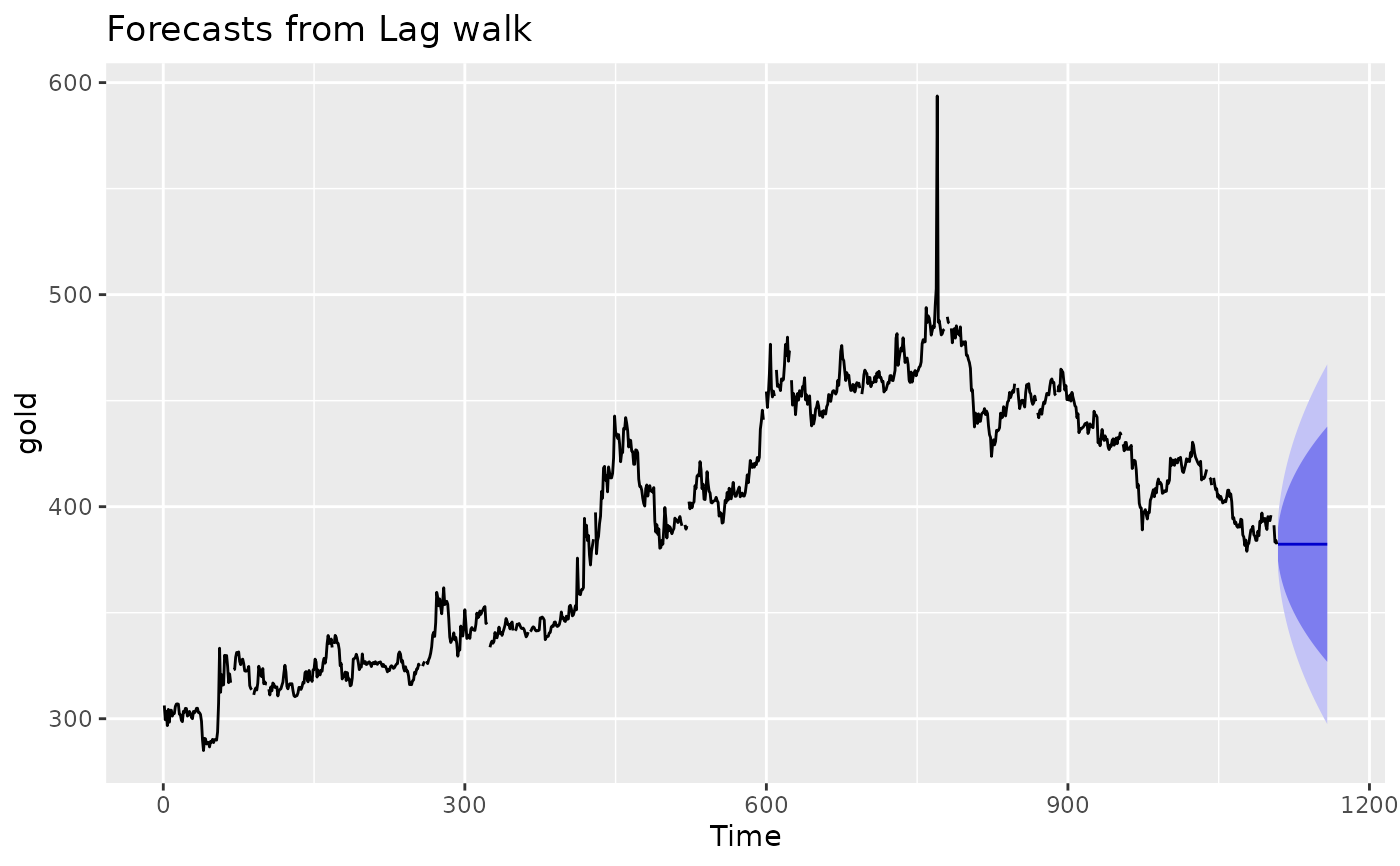

gold_model <- rw_model(gold)

gold_fc1 <- forecast(gold_model, h = 50)

gold_fc2 <- rwf(gold, h = 50)

gold_fc3 <- naive(gold, h = 50)

# Plot the forecasts

autoplot(gold_fc1)

# Drift forecasts

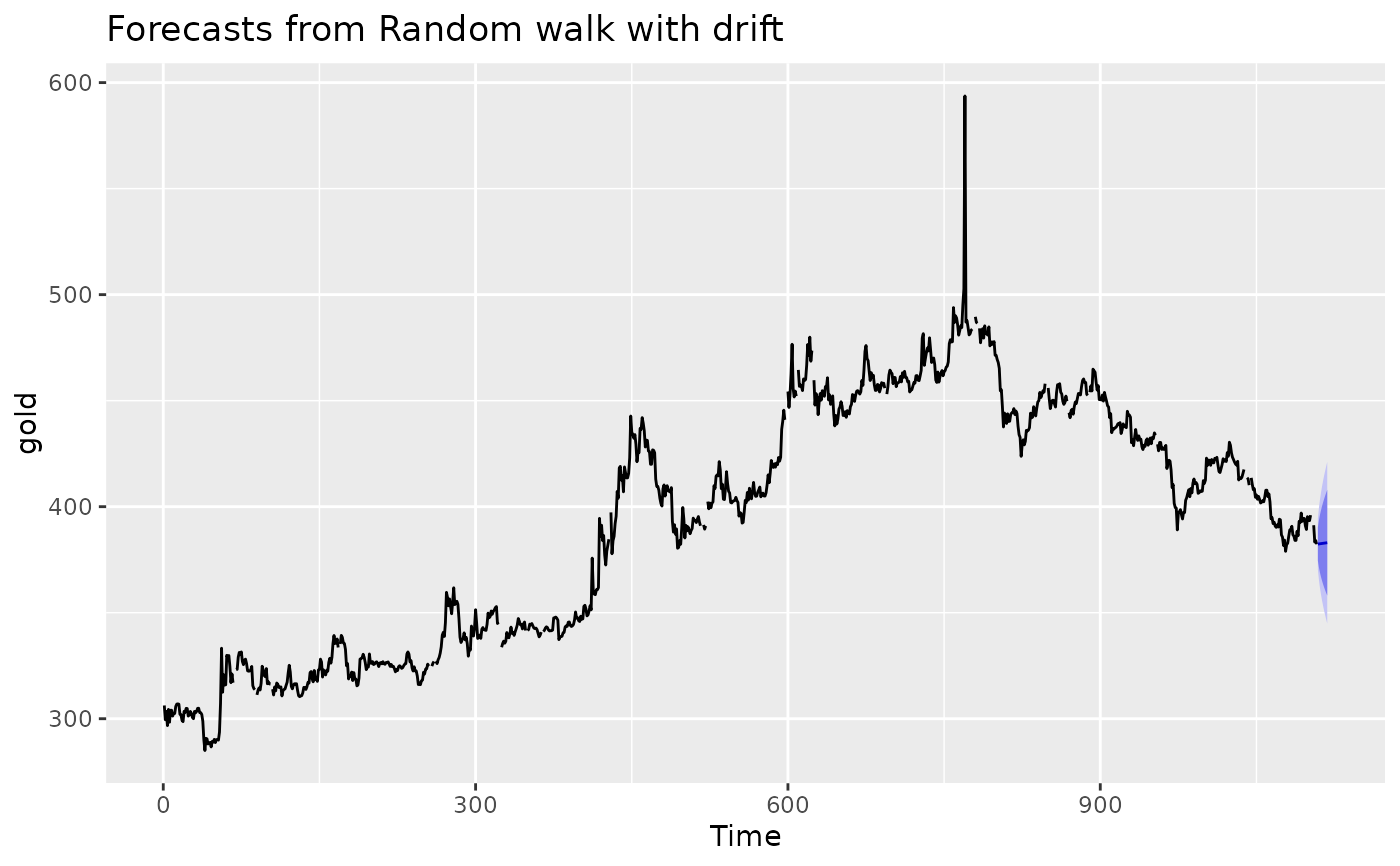

rwf(gold, drift = TRUE) |> autoplot()

# Drift forecasts

rwf(gold, drift = TRUE) |> autoplot()

# Seasonal naive forecasts

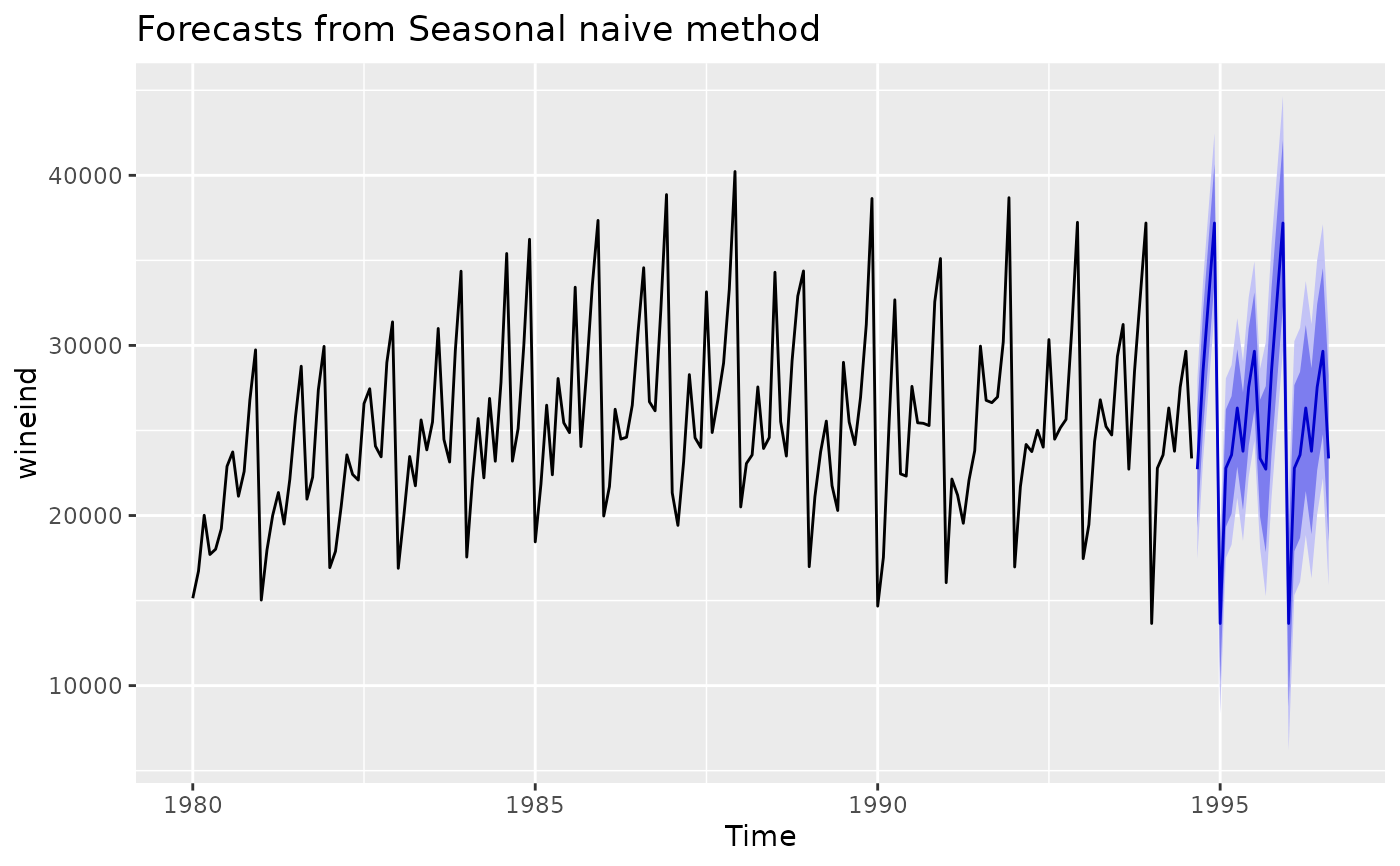

snaive(wineind) |> autoplot()

# Seasonal naive forecasts

snaive(wineind) |> autoplot()