h-step in-sample forecasts for time series models.

Source:R/arfima.R, R/arima.R, R/bats.R, and 4 more

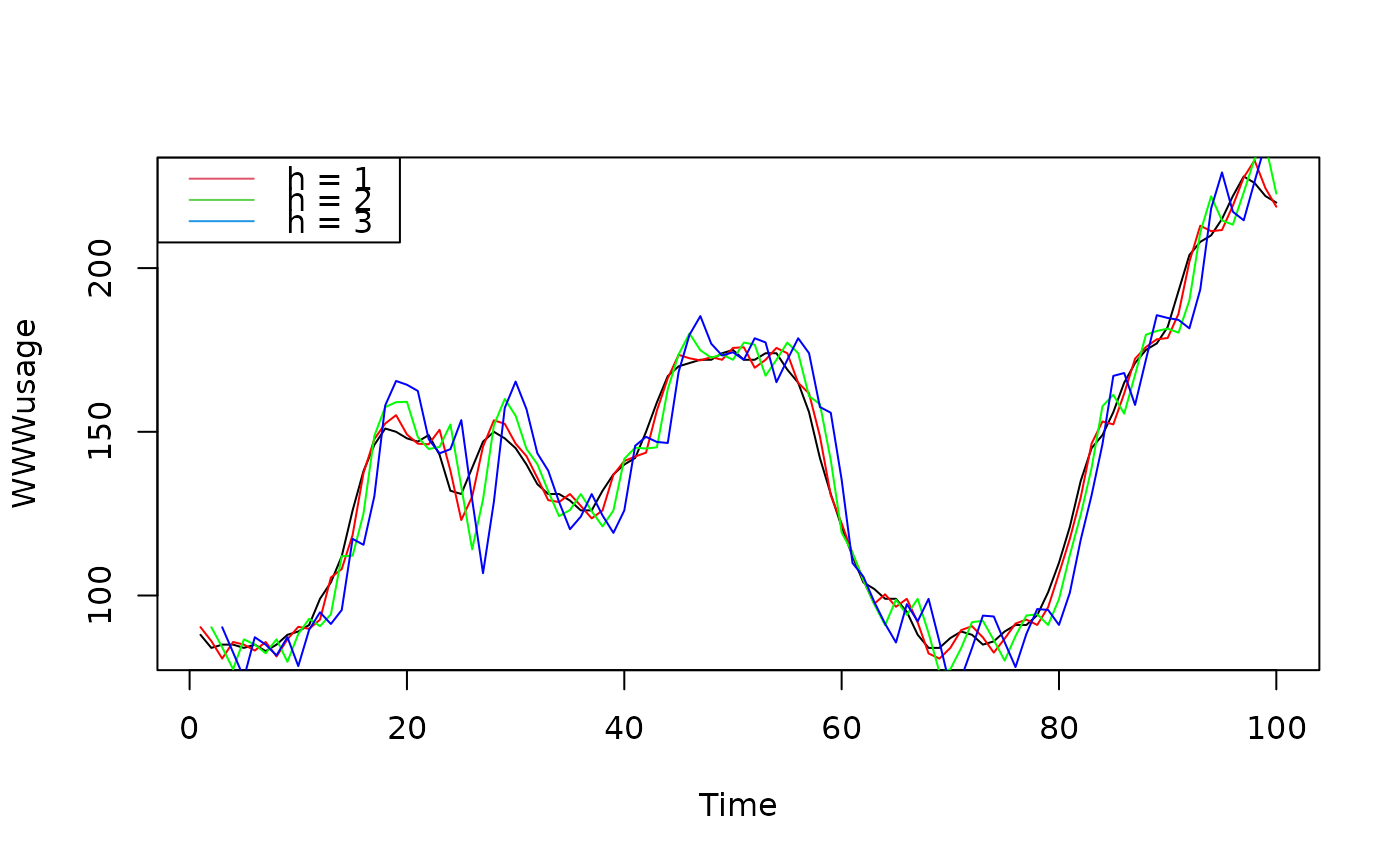

fitted.Arima.RdReturns h-step forecasts for the data used in fitting the model.

Usage

# S3 method for class 'ARFIMA'

fitted(object, h = 1, ...)

# S3 method for class 'Arima'

fitted(object, h = 1, ...)

# S3 method for class 'ar'

fitted(object, ...)

# S3 method for class 'bats'

fitted(object, h = 1, ...)

# S3 method for class 'ets'

fitted(object, h = 1, ...)

# S3 method for class 'modelAR'

fitted(object, h = 1, ...)

# S3 method for class 'nnetar'

fitted(object, h = 1, ...)

# S3 method for class 'tbats'

fitted(object, h = 1, ...)