Check that residuals from a time series model look like white noise

Source:R/checkresiduals.R

checkresiduals.RdIf plot = TRUE, produces a time plot of the residuals, the

corresponding ACF, and a histogram. If test is not FALSE,

the output from either a Ljung-Box test or Breusch-Godfrey test is printed.

Arguments

- object

Either a time series model, a forecast object, or a time series (assumed to be residuals).

- lag

Number of lags to use in the Ljung-Box or Breusch-Godfrey test. If missing, it is set to

min(10, n/5)for non-seasonal data, andmin(2m, n/5)for seasonal data, wherenis the length of the series, andmis the seasonal period of the data. It is further constrained to be at leastdf+3wheredfis the degrees of freedom of the model. This ensures there are at least 3 degrees of freedom used in the chi-squared test.- test

Test to use for serial correlation. By default, if

objectis of classlm, thentest = "BG". Otherwise,test = "LB". Settingtest = FALSEwill prevent the test results being printed.- plot

Logical. If

TRUE, will produce the plot.- ...

Other arguments are passed to

ggtsdisplay().

Examples

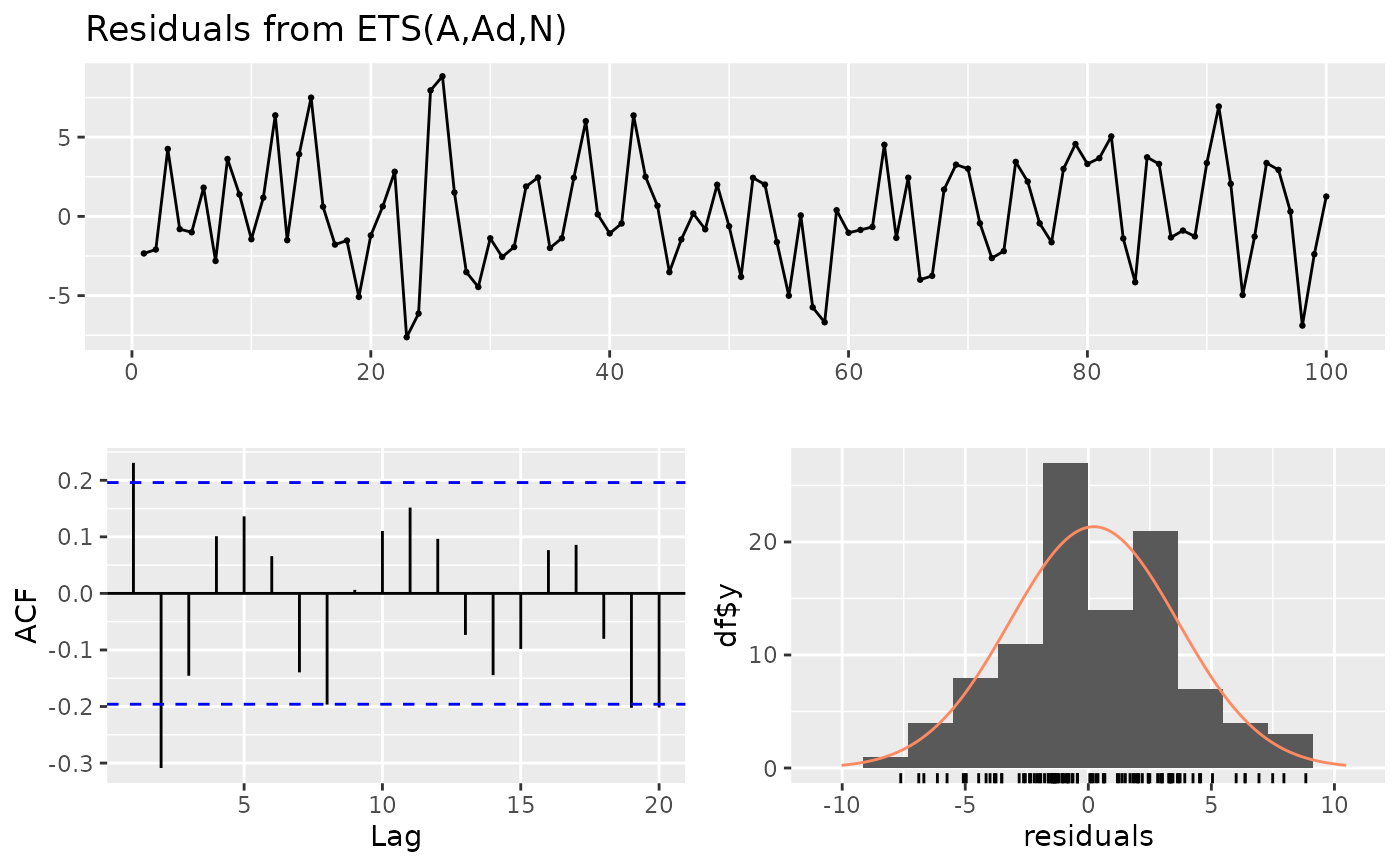

fit <- ets(WWWusage)

checkresiduals(fit)

#>

#> Ljung-Box test

#>

#> data: Residuals from ETS(A,Ad,N)

#> Q* = 28.995, df = 10, p-value = 0.001249

#>

#> Model df: 0. Total lags used: 10

#>

#>

#> Ljung-Box test

#>

#> data: Residuals from ETS(A,Ad,N)

#> Q* = 28.995, df = 10, p-value = 0.001249

#>

#> Model df: 0. Total lags used: 10

#>