ma computes a simple moving average smoother of a given time series.

Details

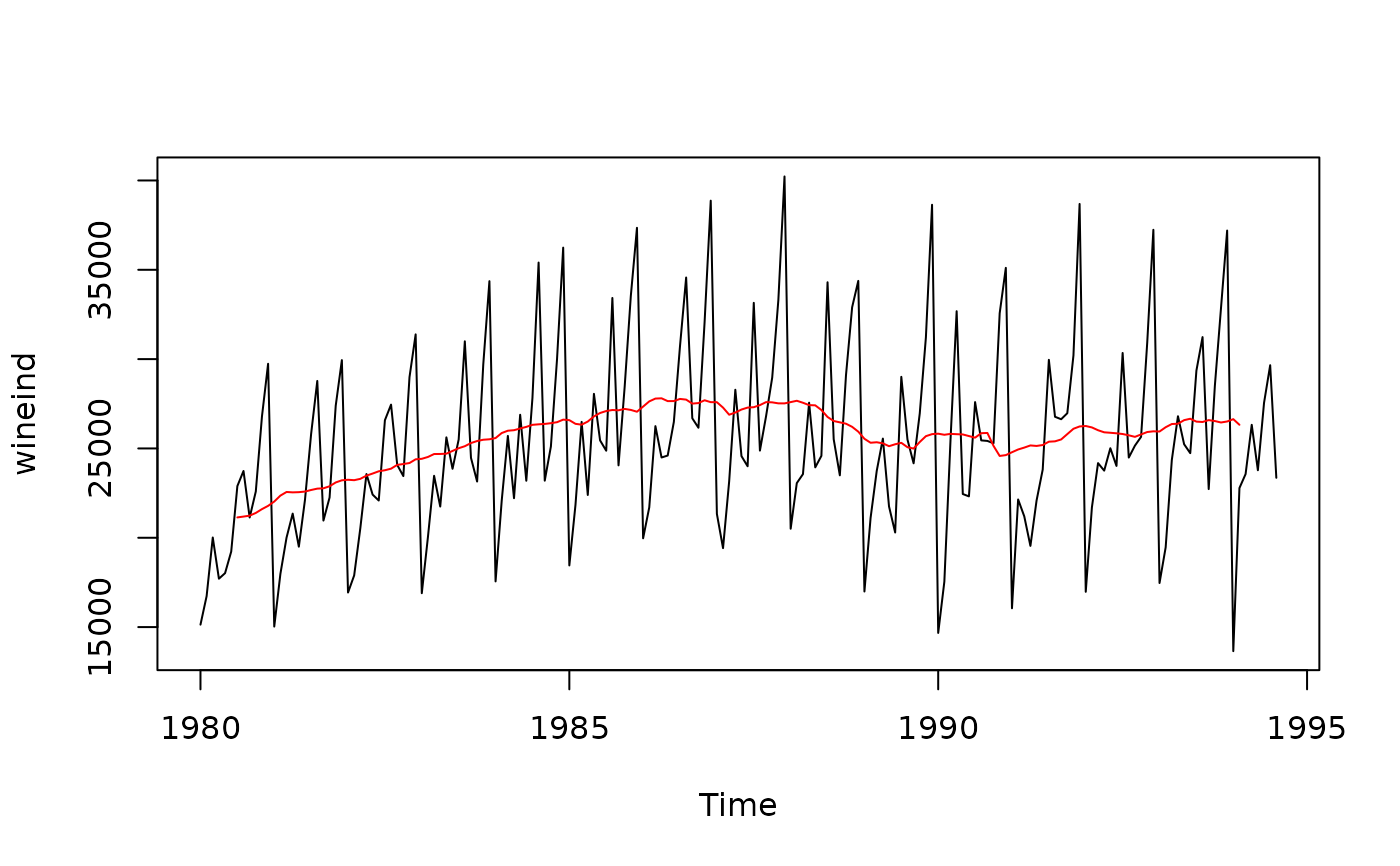

The moving average smoother averages the nearest order periods of

each observation. As neighbouring observations of a time series are likely

to be similar in value, averaging eliminates some of the randomness in the

data, leaving a smooth trend-cycle component.

$$\hat{T}_{t} = \frac{1}{m} \sum_{j=-k}^k y_{t+j}$$

where \(k=\frac{m-1}{2}\).

When an even order is specified, the observations averaged will

include one more observation from the future than the past (k is rounded

up). If centre is TRUE, the value from two moving averages (where k is

rounded up and down respectively) are averaged, centering the moving

average.