Returns forecasts and other information for univariate structural time series models.

Arguments

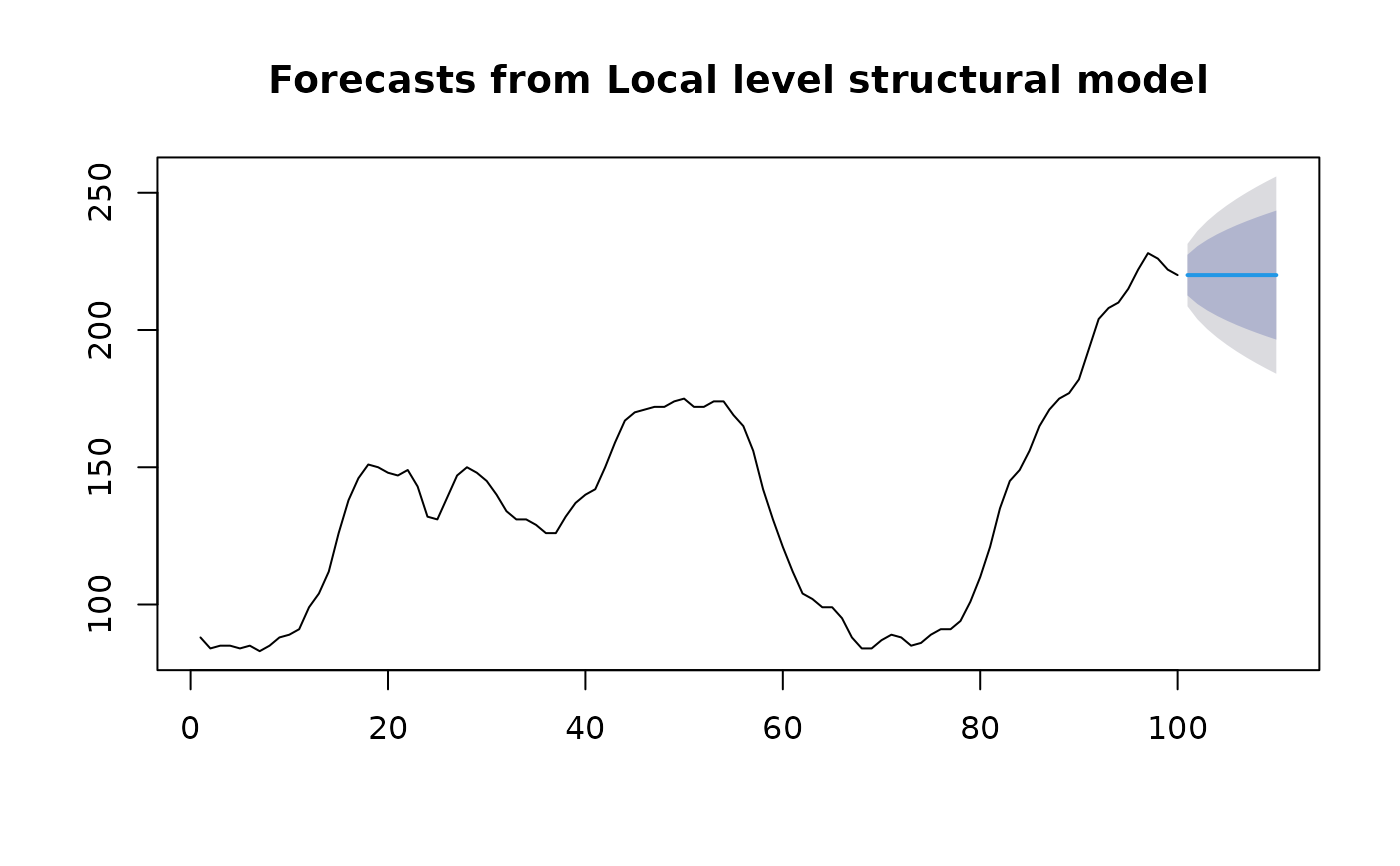

- object

An object of class

StructTS. Usually the result of a call tostats::StructTS().- h

Number of periods for forecasting. Default value is twice the largest seasonal period (for seasonal data) or ten (for non-seasonal data).

- level

Confidence levels for prediction intervals.

- fan

If

TRUE,levelis set toseq(51, 99, by = 3). This is suitable for fan plots.- lambda

Box-Cox transformation parameter. If

lambda = "auto", then a transformation is automatically selected usingBoxCox.lambda. The transformation is ignored if NULL. Otherwise, data transformed before model is estimated.- biasadj

Use adjusted back-transformed mean for Box-Cox transformations. If transformed data is used to produce forecasts and fitted values, a regular back transformation will result in median forecasts. If biasadj is

TRUE, an adjustment will be made to produce mean forecasts and fitted values.- ...

Other arguments are ignored.

Details

This function calls predict.StructTS and constructs an object of

class forecast from the results.

forecast class

An object of class forecast is a list usually containing at least

the following elements:

- model

A list containing information about the fitted model

- method

The name of the forecasting method as a character string

- mean

Point forecasts as a time series

- lower

Lower limits for prediction intervals

- upper

Upper limits for prediction intervals

- level

The confidence values associated with the prediction intervals

- x

The original time series.

- residuals

Residuals from the fitted model. For models with additive errors, the residuals will be x minus the fitted values.

- fitted

Fitted values (one-step forecasts)

The function summary can be used to obtain and print a summary of the

results, while the functions plot and autoplot produce plots of the forecasts and

prediction intervals. The generic accessor functions fitted.values and residuals

extract various useful features from the underlying model.