Returns local linear forecasts and prediction intervals using cubic smoothing splines.

Arguments

- y

a numeric vector or time series of class

ts- h

Number of periods for forecasting

- level

Confidence level for prediction intervals.

- fan

If TRUE, level is set to seq(51,99,by=3). This is suitable for fan plots.

- lambda

Box-Cox transformation parameter. If

lambda="auto", then a transformation is automatically selected usingBoxCox.lambda. The transformation is ignored if NULL. Otherwise, data transformed before model is estimated.- biasadj

Use adjusted back-transformed mean for Box-Cox transformations. If transformed data is used to produce forecasts and fitted values, a regular back transformation will result in median forecasts. If biasadj is TRUE, an adjustment will be made to produce mean forecasts and fitted values.

- method

Method for selecting the smoothing parameter. If

method="gcv", the generalized cross-validation method fromsmooth.splineis used. Ifmethod="mle", the maximum likelihood method from Hyndman et al (2002) is used.- x

Deprecated. Included for backwards compatibility.

Value

An object of class "forecast".

The function summary is used to obtain and print a summary of the

results, while the function plot produces a plot of the forecasts and

prediction intervals.

The generic accessor functions fitted.values and residuals

extract useful features of the value returned by splinef.

An object of class "forecast" containing the following elements:

- model

A list containing information about the fitted model

- method

The name of the forecasting method as a character string

- mean

Point forecasts as a time series

- lower

Lower limits for prediction intervals

- upper

Upper limits for prediction intervals

- level

The confidence values associated with the prediction intervals

- x

The original time series (either

objectitself or the time series used to create the model stored asobject).- onestepf

One-step forecasts from the fitted model.

- fitted

Smooth estimates of the fitted trend using all data.

- residuals

Residuals from the fitted model. That is x minus one-step forecasts.

Details

The cubic smoothing spline model is equivalent to an ARIMA(0,2,2) model but with a restricted parameter space. The advantage of the spline model over the full ARIMA model is that it provides a smooth historical trend as well as a linear forecast function. Hyndman, King, Pitrun, and Billah (2002) show that the forecast performance of the method is hardly affected by the restricted parameter space.

References

Hyndman, King, Pitrun and Billah (2005) Local linear forecasts using cubic smoothing splines. Australian and New Zealand Journal of Statistics, 47(1), 87-99. https://robjhyndman.com/publications/splinefcast/.

Examples

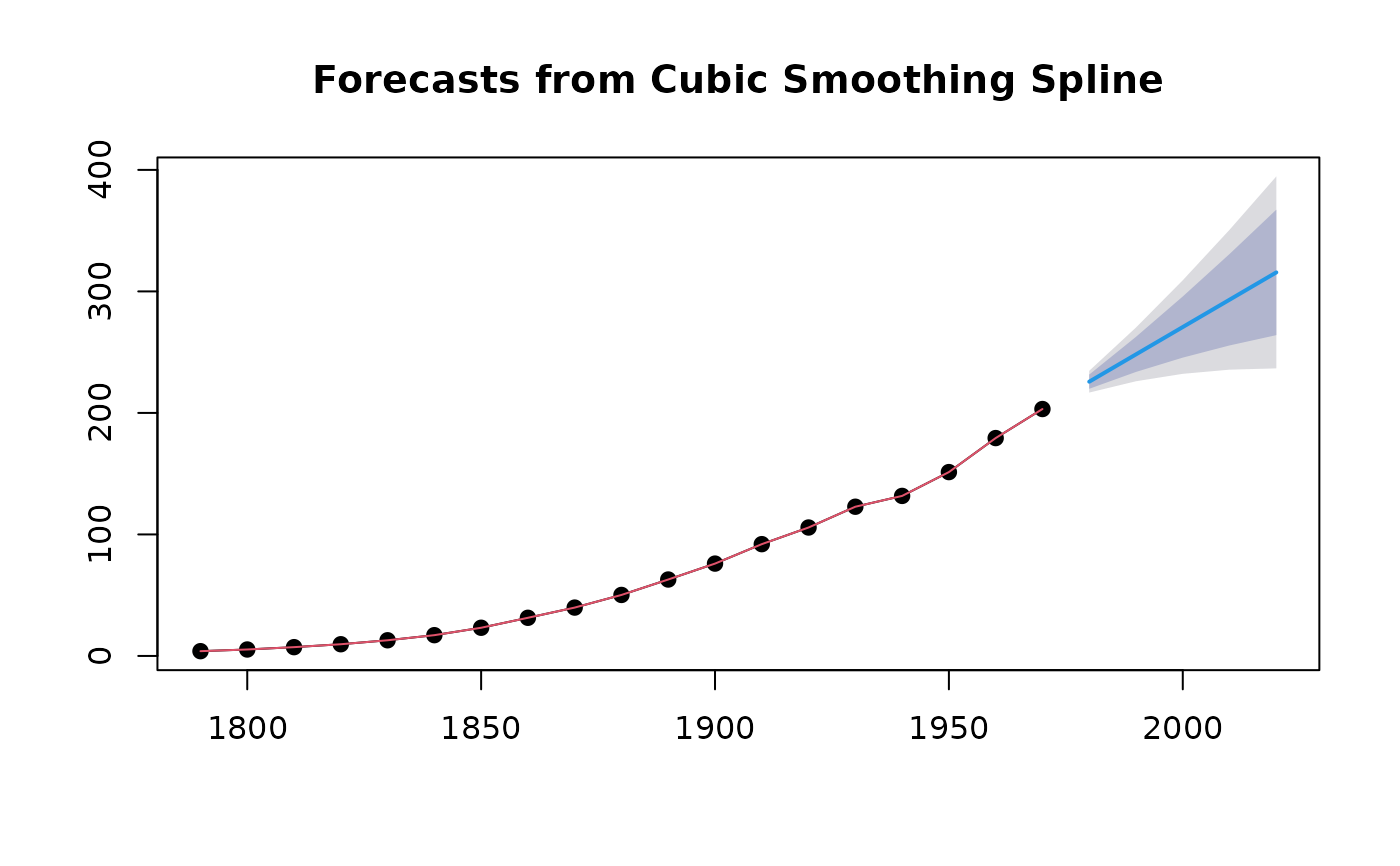

fcast <- splinef(uspop,h=5)

plot(fcast)

summary(fcast)

#>

#> Forecast method: Cubic Smoothing Spline

#>

#> Model Information:

#> $beta

#> [1] 0.0006859

#>

#> $call

#> splinef(y = uspop, h = 5)

#>

#>

#> Error measures:

#> ME RMSE MAE MPE MAPE MASE

#> Training set 0.7704553 4.572546 3.165298 -0.6110405 8.174722 0.04536795

#> ACF1

#> Training set -0.4363661

#>

#> Forecasts:

#> Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

#> 1980 225.6937 219.8454 231.5419 216.7496 234.6378

#> 1990 248.1814 233.7246 262.6382 226.0717 270.2912

#> 2000 270.6692 245.5023 295.8361 232.1798 309.1586

#> 2010 293.1569 255.5241 330.7897 235.6025 350.7113

#> 2020 315.6447 264.0068 367.2826 236.6713 394.6181

summary(fcast)

#>

#> Forecast method: Cubic Smoothing Spline

#>

#> Model Information:

#> $beta

#> [1] 0.0006859

#>

#> $call

#> splinef(y = uspop, h = 5)

#>

#>

#> Error measures:

#> ME RMSE MAE MPE MAPE MASE

#> Training set 0.7704553 4.572546 3.165298 -0.6110405 8.174722 0.04536795

#> ACF1

#> Training set -0.4363661

#>

#> Forecasts:

#> Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

#> 1980 225.6937 219.8454 231.5419 216.7496 234.6378

#> 1990 248.1814 233.7246 262.6382 226.0717 270.2912

#> 2000 270.6692 245.5023 295.8361 232.1798 309.1586

#> 2010 293.1569 255.5241 330.7897 235.6025 350.7113

#> 2020 315.6447 264.0068 367.2826 236.6713 394.6181